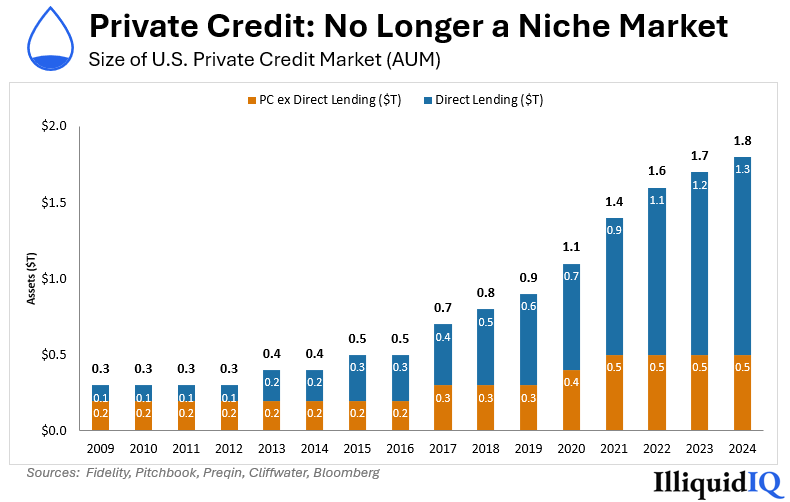

- The U.S. private credit market is $1.8TN+ of assets under management and has grown at a ~14% rate over the past decade.

- High profile bankruptcies and valuation write downs in the private credit market have caused investor fear, uncertainty, and doubt.

- IlliquidIQ is an independent private markets data and content platform focused on bringing enhanced transparency to the private credit market.

Overview

Private credit has had a remarkable decade. What was once a niche strategy — non-bank lenders making loans to middle-market companies — has grown into a market with ~$1.8TN in assets under management in the United States.

Many point to the Dodd-Frank Wall Street Reform and Consumer Protection Act as the first catalyst for the private credit market. Passed in 2010, it was a sweeping federal law that overhauled the U.S. banking regulatory framework following the 2008 financial crisis.

Its goals? Preventing future taxpayer funded bailouts, protect consumers, and inhibit excessive risk taking. Ten years later, the degree to which it has achieved those is a question we'll leave for the policymakers and academics.

But one thing is certain: it has provided a catalyst for private credit lending. The market has expanded at a ~14.5% compound annual growth rate over the past decade. While the private credit fundraising environment has been challenging over the past ~12 months, the long-term growth trajectory of the asset class remains fully intact.

The Private Credit Value Proposition

The credit fund managers' pitch to borrowers goes something like this: more flexibility on terms relative to bank financing, better certainty of execution, and, in many private equity backed transactions, a relationship-oriented strategy that can be critical when navigating bumps in the road.

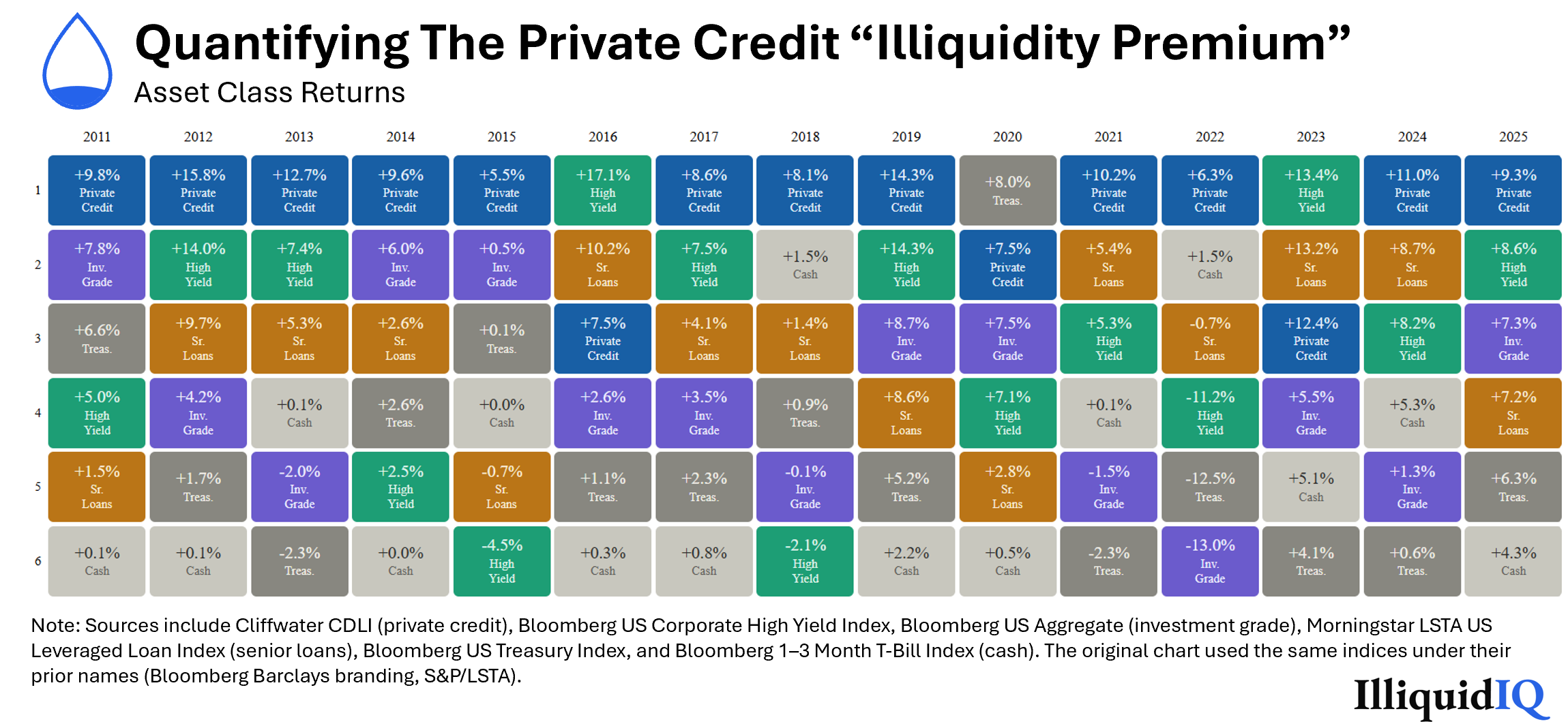

The fund managers' pitch to private credit investors goes something like this: higher yields than publicly traded bonds, lower volatility, and strong downside protection given most loans are senior secured. In other words, provide your fund manager capital, sit tight, and over a 5-7 year period you'll reap the rewards of the so-called "illiquidity premium" — the extra risk adjusted return for your patience.

The results have been hard to deny — private credit returns have beaten those of other competing asset classes, notably Leveraged Loans and High Yield Bonds, by a sizeable margin in 12 of the last 15 years.

But how are private credit indices (like the Cliffwater CDLI index above) actually calculated? Is the asset class truly less volatile than its more liquid counterparts? Or does the lack of real time market data just mask underlying volatility?

The Problem

Private credit is called "private" for a reason. The underlying loans that private credit firms underwrite are not traded. The borrowers are not public companies with quarterly earnings releases. The valuation practices employed by fund managers to calculate performance metrics are, to varying degrees, distinct and opaque.

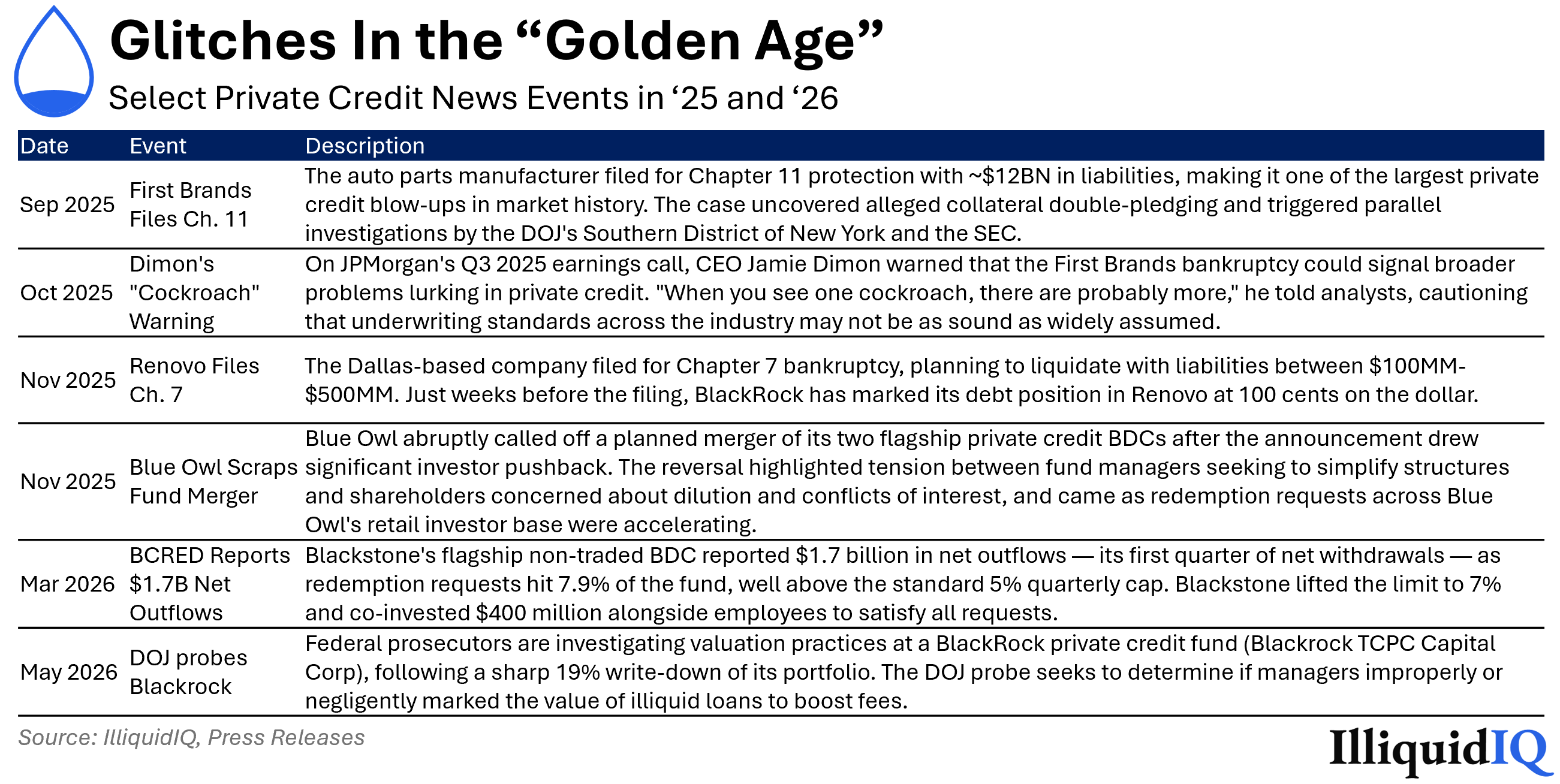

That lack of transparency is a feature, not a bug. But it is also what has caused much of the controversy and confusion about the asset class over the past 12-18 months. From the high-profile bankruptcy of First Brands in September 2025 to the record outflows that non-traded BDCs and interval funds have seen so far in 2026, there have been and will continue to be bumps in the road.

With little data publicly available for someone to actually verify what's going on in the market, it's no surprise that headlines warning of "systemic risk" or "contagion" have grabbed the attention of many.

In response to these (oftentimes sensationalist) headlines, private credit fund managers have gone out of their way to reassure investors of the resilience of their portfolios, their strong liquidity profile, and the overall durability of the asset class.

We're not here to pick sides.

Not all private credit loans were made to software companies whose business models are going to be upended by AI in the next six months. Not all private credit portfolio valuations are inflated. Not all private credit loans are leveraged loans made to sub-investment grade issuers.

But we are here to present the facts.

The private credit landscape is already too big to ignore. It gets more complex by the week and headlines that lump the entire private credit ecosystem into one single "asset class" do a disservice to everyone. The details matter now more than ever.

Our goal: to keep you informed of the latest developments in private credit using a data driven approach.

What We're Building

Data: comprehensive data sets and dashboards that capture the key metrics moving private credit markets. Our focus will initially be on direct lending in the middle market. For a sneak peek, look at our first data set — the non-traded BDC and interval fund redemption tracker.

Content: private credit can seem incredibly complex. We'll break it down with research and analysis that purges the jargon and presents the facts in their simplest form. At the end of the day, most of it boils down to "napkin math".

What IlliquidIQ Is Not

We are not a ratings agency. We do not issue investment recommendations. We are not affiliated with any fund manager, broker-dealer, or distributor. While we use AI tools to aggregate data and edit (not author) content, everything posted on this website is verified by our team. Nothing on this platform is investment advice and is intended solely for informational purposes.

Thank you for your interest. We'd love to hear from you — reach us at inquiry@illiquidiq.com.

— The IlliquidIQ Team